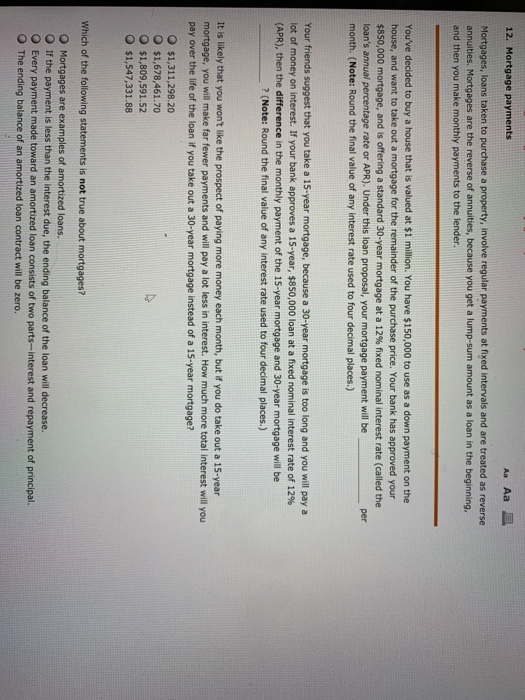

According to a 2015 short article in the, in 2014, about 12% of the United States HECM reverse mortgage debtors defaulted on "their property taxes or homeowners insurance" a "fairly high default rate". In the United States, reverse mortgage debtors can face foreclosure if they do not keep their homes or keep up to date on property owner's insurance and real estate tax.

On 25 April 2014, FHA modified the HECM age eligibility requirements to https://www.globenewswire.com/news-release/2020/05/07/2029622/0/en/U-S-ECONOMIC-UNCERTAINTIES-DRIVE-TIMESHARE-CANCELLATION-INQUIRIES-IN-RECORD-NUMBERS-FOR-WESLEY-FINANCIAL-GROUP.html extend particular defenses to spouses younger than age 62. Under the old guidelines, the reverse home loan could only be composed for the partner who was 62 or older. If the older spouse died, the reverse home loan balance became due and payable if the more youthful enduring partner was left off of the HECM loan.

This often developed a significant challenge for spouses of deceased HECM debtors, so FHA modified the eligibility requirements in Mortgagee Letter 2014-07. Under the new standards, spouses who are younger than age 62 at the time of origination keep the protections offered by the HECM program if the older partner who got the home mortgage passes away.

For a reverse home mortgage to be a feasible financial choice, existing mortgage balances generally must be low enough to be settled with the reverse mortgage earnings - how do bad credit mortgages work. However, customers do have the choice of paying for their existing home mortgage balance to receive a HECM reverse home mortgage. The HECM reverse home mortgage follows the basic FHA eligibility requirements for home type, indicating most 14 family houses, FHA approved condos, and PUDs qualify.

Prior to starting the loan procedure for an FHA/HUD-approved reverse home loan, applicants need to take an authorized counseling course. An authorized therapist ought to assist explain how reverse mortgages work, the financial and tax implications of taking out a reverse mortgage, payment alternatives, and costs connected with a reverse home mortgage. The counseling is meant to secure debtors, although the quality of therapy has been slammed by groups such as the Consumer Financial Security Bureau.

What Banks Give Mortgages For Live Work for Dummies

On March 2, 2015, FHA implemented brand-new standards that need reverse home mortgage candidates to go through a monetary evaluation. Though HECM debtors are not needed to make monthly home loan payments, FHA wishes to make sure they have the monetary ability and willingness to keep up with real estate tax and house owner's insurance coverage (and any other appropriate residential or commercial property charges).

Prior to 2015, a Lender might not decline a demand for a HECM as the requirement is age 62+, own a home, and fulfill initial debt-to-equity requirements. With FA, the loan provider may now force Equity "reserved" rules and amounts that make the loan difficult; the like a declination letter for poor credit.

Acceptable credit - All housing and installment financial obligation payments must have been made on time in the last 12 months; there are no more than two 30-day late mortgage or installation payments in the previous 24 months, and there is no significant bad credit on revolving accounts in the last 12 months.

If no extenuating circumstances can be recorded, the debtor might not qualify at all or the loan provider might require a big quantity of the principal limit (if available) to be sculpted out into a Life Span Reserve (LESA) for the payment of residential or commercial property charges (real estate tax, homeowners insurance coverage, etc.).

The fixed-rate program comes with the security of an interest rate that does not alter for the life of the reverse home loan, but the rates of interest is generally greater at the start of the loan than a comparable adjustable-rate HECM. Adjustable-rate reverse home loans typically have rate of interest that can change on a monthly or yearly basis within certain limits.

A Biased View of How Do Rehab Mortgages Work

The preliminary rates of interest, or IIR, is the real note rate at which interest accrues on the outstanding loan balance on an annual basis. For fixed-rate reverse home loans, the IIR can never ever alter. For adjustable-rate reverse home mortgages, the IIR can alter with program limits up to a lifetime rate of interest cap.

The EIR is frequently different from the actual note rate, or IIR. The EIR does not determine the amount of interest that accrues on the loan balance (the IIR does that). The overall swimming pool of cash that a customer can receive from a HECM reverse mortgage is called https://www.facebook.com/ChuckMcDowellCEO/ the principal limit (PL), which is computed based on the optimum claim amount (MCA), the age of the youngest debtor, the predicted rate of interest (EIR), and a table to PL aspects released by HUD.

Most PLs are normally in the range of 50% to 60% of the MCA, but they can in some cases be greater or lower. The table below gives examples of principal limits for different ages and EIRs and a property worth of $250,000. Borrower's age at origination Expected interest rate (EIR) Principal limitation aspect (as of Aug.

5% 0. 478 $119,500 65 7. 0% 0. 332 $83,000 75 5. 5% 0. 553 $138,250 75 7. 0% 0. 410 $102,500 85 5. 5% 0. 644 $161,000 85 7. 0% 0. 513 $128,250 The primary limitation tends to increase with age and decrease as the EIR rises. To put it simply, older debtors tend to receive more money than younger customers, however the overall amount of cash offered under the HECM program tends to reduce for all ages as interest rates rise.

Any extra earnings readily available can be dispersed to the debtor in numerous methods, which will be detailed next. The cash from a reverse home mortgage can be dispersed in 4 methods, based upon the borrower's financial requirements and goals: Lump amount in cash at settlement Month-to-month payment (loan advance) for a set variety of years (term) or life (tenure) Credit line (similar to a house equity credit line) Some mix of the above Note that the adjustable-rate HECM provides all of the above payment alternatives, however the fixed-rate HECM just provides lump sum.

The 5-Minute Rule for What Work Is Mortgages?

This indicates that customers who go with a HECM line of credit can potentially get to more cash in time than what they initially got approved for at origination. The line of credit development rate is identified by including 1. 25% to the preliminary rate of interest (IIR), which indicates the line of credit will grow quicker if the interest rate on the loan increases.

Because numerous debtors were taking full draw swelling sums (typically at the encouragement of lending institutions) at closing and burning through the cash rapidly, HUD sought to safeguard borrowers and the practicality of the HECM program by limiting the quantity of earnings that can be accessed within the very first 12 months of the loan.

Any staying offered proceeds can be accessed after 12 months. If the total obligatory obligations surpass 60% of the principal limitation, then the customer can draw an additional 10% of the primary limitation if available. The Real Estate and Economic Healing Act of 2008 supplied HECM mortgagors with the chance to purchase a new principal home with HECM loan proceeds the so-called HECM for Purchase program, effective January 2009.